We can diligently eat healthy food and exercise regularly to maintain good health, but preparing for the unexpected may be a more difficult task. That’s where health insurance comes into play.

Health insurance is essential because you never know what can happen, accidents, and illness can strike at any time. If you aren’t protected, not only could you miss out on getting the right treatment, it cost you more money than you have.

Before you embark on finding the health insurance you need in Singapore, here are 5 quick things you need to know.

MediShield Life is a basic health insurance plan for Singapore Citizens and Permanent Residents (PR). MediShield Life offers protection regardless of age or health condition for large hospital bills. MediShield also covers selected costly outpatient treatments, such as dialysis and chemotherapy for cancer. Kidney Dialysis claim limit is $1,000 per month whilst chemotherapy claim limit is $3,000 per month.

MediShield Life is mandatory insurance for Singapore Citizens and Permanent Residents, and the premiums for MediShield Life can be paid using CPF Medisave funds or cash.

Note that MediShield Life is a basic health insurance. Its coverage for outpatient cancer treatments is limited and its claim limits would often not be sufficient for stays in private hospitals. If you plan to use an A/B1-type ward in a public hospital or go to a private hospital for your future hospitalisations, you would need to consider other types of health insurance to enhance your coverage.

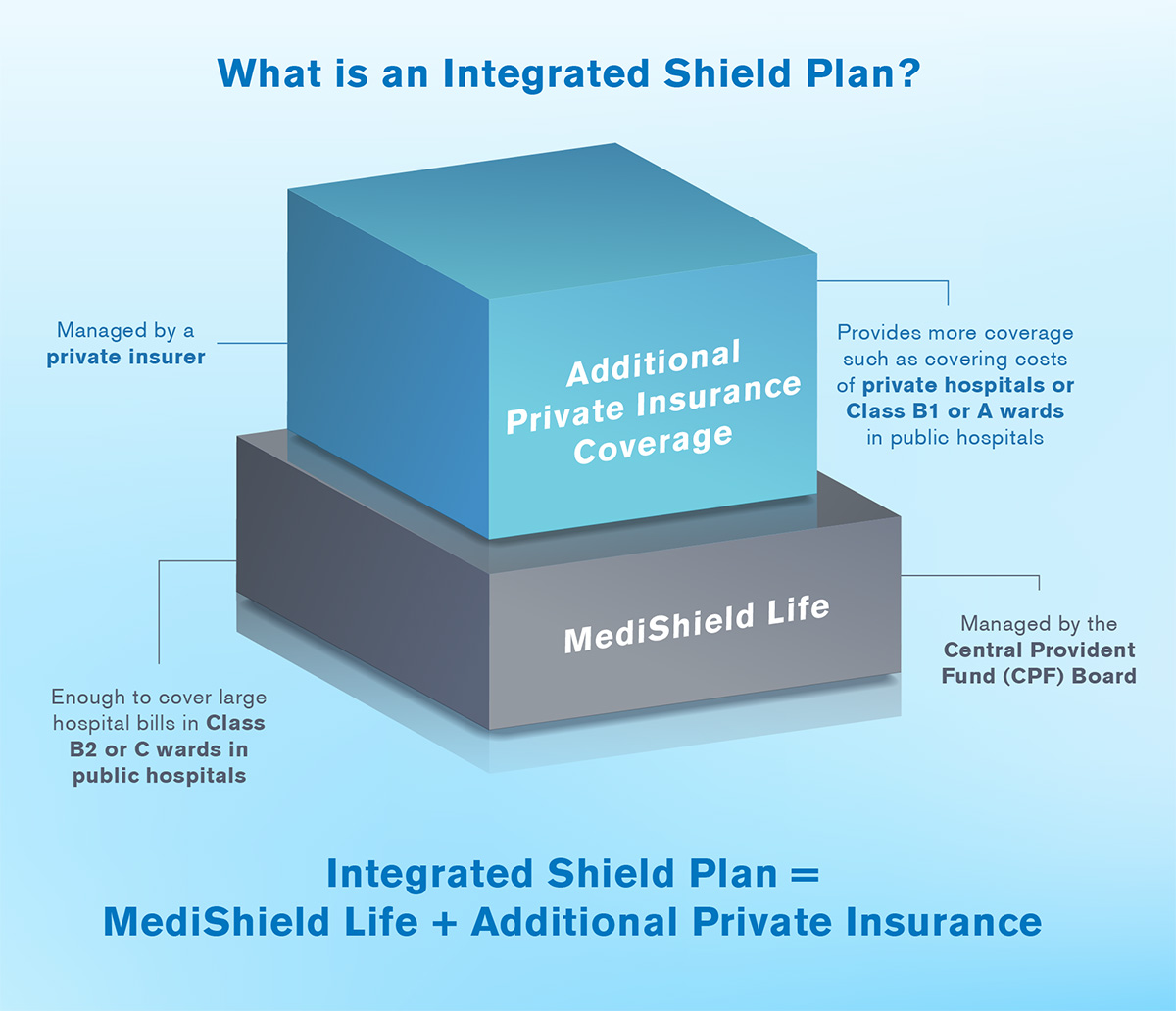

An Integrated Shield Plan (IP) combines MediShield Life with the additional coverage provided by private insurers. There are many variations of these. Still, they all extend the coverage of MediShield Life to cover Class B1 and A in public hospitals, as well as costs in private hospitals.

( Source: www.moh.gov.sg/medishield-life/about-integrated-shield-plans )

Besides Medishield Life which covers stays in B2/C ward, there are a few Integrated Shield Plans:

1) Class B1 Plan: provides additional coverage beyond MediShield Life coverage, targeted at stays in Class B1 wards in public hospitals

2) Class A Plan: provides coverage for stays at Class A wards in public hospitals

3) Private Hospitals Plan: coves treatments and stays in private hospitals in Singapore

The MediShield Life component of your Integrated Shield Plan is fully payable by MediSave.

The additional private insurance component of basic plan is also payable by MediSave, but only up to the following Additional Withdrawal Limits:

- $300 per year for those at age 40 years and below on their next birthday

- $600 per year for those at age 41 to 70 years on their next birthday

- $900 per year for those at age 71 years and above on their next birthday

Any excess and riders would need to be paid in cash.

Aside from MediShield Life, there are a few other health insurance options for Singapore citizens and Permanent Residents. These include:

Domestic Health Plan – covers hospitalisation expenses for people who cannot buy Integrated Shield Plan, for example, foreigners or Singaporeans/PR who have received rejection from Integrated Shield Plan application before.

International Health Plan – provides comprehensive coverage including inpatient, outpatient, wellness, dental and maternity benefits. Such a plan is suitable for expatriates and people that travel overseas often.

Hospital Cash Insurance – pays you a fixed amount of money for each day you spend in the hospital. It’s typical for the amount paid out to be more or less than your actual medical costs.

Critical Illness Insurance – pays a lump sum if you are diagnosed with any of the illnesses covered.

Disability Income Insurance – pays you a fixed amount each month to replace the income you lose if you cannot work due to an illness or accident.

Severe Disability or Long Term Care Insurance – pay for the care you need if you’re severely disabled. One such insurance is the ElderShield which provides monthly payout of $400 for up to 6 years to severely disabled elderly who need long-term care. ElderShield will be enhanced to CareShield Life in 2020, which pays out higher $600+ monthly for life.

As you research which plan is best for you, it helps to understand key terms associated with health insurance.

Premiums

The amount paid to keep your health insurance going is known as a premium. It may be a lump sum (single premium) or in smaller amounts (regular premiums) monthly, quarterly, or annually.

Deductible

How much you have to pay first for your medical expenses before your health insurance makes a payout. It’s only necessary to pay the deductible once in a policy year.

Co-insurance

This is the dollar amount you have to co-pay or split the cost with the insurer after you pay the deductible. Typically expressed as a percentage. If you have a co-insurance of 20%, you will pay 20% of the cost after the deductible, for example.

Claim Limits

These are the limits to what you can claim under a policy.

Pre-existing Condition

A pre-existing condition is any health condition that was present prior to your new insurance coverage

While it may seem like there are way too many choices, and coverage to understand, you only need a basic idea of what you want to get started. Understanding the limits of MediShield Life is a great starting point. Once you know the limitation, you can pick an IP that fits your situation best.

You should also consider specialised health insurance such as Critical Illness Insurance to adequately covers medical treatment you need to get well again.

There are a few things that will help you in the decision making process:

- Annual coverage limit

- Whether you prefer to be treated at public or private hospital

- Your preferred type of ward stay in a public hospital

- Pre- and post-hospitalisation coverage

- Price of premiums

Need someone experienced in health insurance to assist you to find and decide on the health insurance plan your need? Feel free to reach out to us via the form below.

Policy Comparison and Unbiased Advice